In This Guide

- Understanding California Probate

- What Happens to the House During Probate?

- How Long Does California Probate Take?

- Common Challenges for Bay Area Executors and Families

- Proposition 19 and Tax Considerations

- Options for an Inherited Bay Area House

- Frequently Asked Questions About Probate and Inherited Houses

- Help With a Bay Area Probate or Inherited House

When a family member passes away and leaves behind a house, the people responsible for the estate often face many unfamiliar decisions at once.

You may be grieving while also trying to protect the property, understand legal documents, communicate with family members, pay ongoing expenses, and decide what should happen to the home.

Questions can arise quickly:

- Does the house have to go through probate?

- Does having a will avoid probate?

- Can the house be sold before probate is completed?

- Who pays the mortgage, property taxes, insurance, and maintenance?

- What happens if the property has a reverse mortgage?

- Will Proposition 19 increase the property taxes?

- What if family members disagree about whether to keep or sell the house?

- Does the estate need to repair and clean out the property before selling?

- Is it better to list the house or sell it directly in its current condition?

These questions can be especially important in the San Francisco Bay Area, where an inherited home may be worth a substantial amount but also come with high carrying costs, expensive repairs, tenant issues, or decades of accumulated belongings.

Throughout this guide, I’ll focus on probate and inherited-house issues commonly encountered by families in San Mateo County, Santa Clara County, Alameda County, San Francisco County, Contra Costa County, and other Bay Area communities.

A property purchased many years ago may have a low property-tax basis, but inheritance can create new tax considerations. A vacant home may require different insurance coverage and regular maintenance. An older property may also have deferred repairs, unpermitted improvements, code violations, or outdated systems.

At the same time, family members may live in different cities or states and have different goals. One heir may want to keep the property as a rental, another may want to move into it, and another may prefer to sell so the estate can be distributed.

There is no single solution that is right for every family.

This guide explains the California probate and inherited-property process from a practical real estate perspective. It is intended for executors, administrators, personal representatives, successor trustees, heirs, and beneficiaries trying to understand their options.

It also explains the differences between keeping the property, listing it on the open market, and selling it directly in its present condition. Understanding these choices can help the family compare price, expenses, timing, risk, and likely net proceeds.

1. Understanding California Probate

Probate is the court-supervised process used to settle a person’s estate after death.

The process may involve:

- Determining whether a will is valid

- Appointing someone to manage the estate

- Identifying estate assets

- Notifying heirs, beneficiaries, and creditors

- Paying valid debts, taxes, and expenses

- Managing or selling real estate

- Distributing the remaining property

- Closing the estate

When formal probate is necessary, the California Superior Court appoints a personal representative to manage the estate. This person is usually called an executor when named in a will and an administrator when there is no will or the named executor cannot serve. (Self-Help Guide to the California Courts)

Does Having a Will Avoid Probate?

A will does not necessarily avoid probate.

A will generally states who should inherit the deceased person’s property and who should serve as executor. However, if the home remained in the deceased person’s individual name and no other transfer method applies, a probate proceeding may still be required.

The person named in the will does not automatically receive full authority over the estate immediately after death. That person generally must petition the court, be appointed as personal representative, and receive the required court documents before acting on behalf of the estate.

What Happens If There Is No Will?

When someone dies without a valid will, they are said to have died intestate.

California’s intestate succession laws determine who inherits the estate, and the probate court may appoint an administrator to manage it.

The absence of a will can create additional complications, including:

- Disagreements over who should serve as administrator

- Difficulty identifying all legal heirs

- Missing or out-of-state heirs

- Family disputes over the inherited house

- Delays in collecting the necessary information

These issues are common in the Bay Area, where family members may live in different states or countries and the home may represent a large portion of the estate’s value.

Not Every Inherited House Requires Formal Probate

An inherited house and a probate house are not necessarily the same thing.

Whether formal probate is required depends on several factors, including:

- How title was held

- Whether the property was in a living trust

- Whether there was a surviving joint owner

- Whether a transfer-on-death deed or another transfer arrangement applies

- The type and value of the estate under current California law

California also provides simplified transfer procedures for some estates, and the applicable value limits can change. Families should not assume that formal probate is—or is not—required based only on the existence of a will or the estimated value of the home. (Self-Help Guide to the California Courts)

Does a Living Trust Avoid Probate?

A properly prepared and funded living trust can often allow a successor trustee to manage or transfer the house without formal probate.

However, simply creating a trust document is not enough.

A common problem occurs when someone signs a living trust but never records a deed transferring the home into the trust. After the owner’s death, the family may discover that title still remains in the owner’s individual name.

Other title problems may include:

- An outdated deed

- A deceased joint owner who was never removed from title

- A misspelled or inconsistent owner name

- A transfer that was signed but never recorded

- Conflicting estate-planning documents

- Ownership shared with another person

Because the correct procedure depends on title and the estate documents, one of the family’s first steps should be to confirm the property’s recorded ownership and review it with an appropriate attorney.

What Are Letters Testamentary or Letters of Administration?

After the court appoints the personal representative, the court issues documents commonly referred to as Letters.

Letters Testamentary are generally issued to an executor named in a will. Letters of Administration are generally issued to an administrator.

Banks, title companies, escrow officers, and other institutions may request certified copies of these documents as evidence that the personal representative has authority to act for the estate.

What Is a Probate Referee?

A Probate Referee is appointed to appraise certain non-cash estate assets, including real property.

The Probate Referee’s valuation is generally based on the property’s fair market value as of the date of death. However, that appraisal is not necessarily the same as the price the home will ultimately sell for.

The actual sale price can be affected by:

- The property’s physical condition

- Deferred repairs

- Tenant or occupancy issues

- Market conditions at the time of sale

- Buyer demand

- Financing availability

- How widely the property is marketed

- The terms and certainty of the offer

A Realtor® or appraiser can help the estate understand the property’s current market value, while the Probate Referee’s valuation serves a different role in the estate-administration process.

What Is the Independent Administration of Estates Act?

The Independent Administration of Estates Act, commonly called the IAEA, may give the personal representative authority to handle certain estate transactions with less direct court supervision.

A personal representative may receive full or limited authority.

With full authority, the representative can often sell estate real property without a court-confirmation hearing, although notice requirements and other legal procedures may still apply.

With limited authority, additional court supervision and confirmation may be required. The exact process depends on the authority granted, the terms of the will, court orders, and the facts of the sale.

The estate attorney and escrow or title professionals should confirm the representative’s authority before the property is marketed or a closing date is promised.

2. What Happens to the House During Probate?

The house does not necessarily transfer to the heirs immediately after death.

During probate, the property remains an estate asset, and the personal representative is responsible for protecting and managing it. A trustee has similar practical responsibilities when the property is held in a trust.

The property continues to generate expenses even if no one is living there.

Common expenses include:

- Mortgage payments

- Property taxes

- Homeowners or vacant-property insurance

- Utilities

- HOA dues

- Landscaping and yard care

- Security

- Emergency repairs

- Cleaning and debris removal

If the estate has little available cash, these expenses can create financial pressure. Family members may disagree over who should advance the money or whether additional funds should be spent repairing the home.

Executor’s First Steps for an Inherited House

Every case is different, but common first steps include:

- Secure the property. Confirm that doors, windows, gates, garages, and outbuildings are secured.

- Locate the estate documents. Look for the will, trust, amendments, deeds, mortgage statements, insurance records, and property-tax bills.

- Confirm the recorded ownership. The deed may determine whether probate, trust administration, or another transfer procedure applies.

- Contact the insurance company. Notify the carrier of the owner’s death and determine whether the current policy remains appropriate.

- Identify all loans and liens. Determine whether the property has a conventional mortgage, reverse mortgage, home-equity line, tax lien, judgment, or other secured debt.

- Maintain essential utilities. Electricity, water, heat, security systems, or landscaping may need to remain active to protect the property.

- Forward the mail. Mail may reveal bills, insurance notices, loan statements, or other important obligations.

- Protect records and valuables. Avoid distributing, selling, or discarding personal property until the appropriate representative and attorney determine what can be done.

- Document expenses. Keep receipts and records of payments made for the property or estate.

- Speak with the estate attorney. Confirm the representative’s legal authority before signing contracts, removing property, or making major financial decisions.

Insurance and Vacant-Property Risk

Homeowners insurance should be addressed promptly.

A policy written for an owner-occupied home may not provide the same protection after the owner dies or the property becomes vacant for an extended period. The personal representative or trustee should contact the insurer and accurately explain the property’s occupancy status.

Vacant inherited homes may be exposed to:

- Break-ins

- Vandalism

- Water leaks

- Fire

- Illegal dumping

- Trespassing

- Pest problems

- Overgrown landscaping

- Code violations

Someone should inspect the property regularly, even when the executor or heirs live out of the area.

What If Someone Is Living in the House?

An heir, family member, tenant, caregiver, or other occupant may already be living in the property.

The owner’s death does not automatically erase an existing tenancy or give the family an immediate right to remove an occupant. California and local Bay Area rental laws may affect the estate’s options.

Questions may arise over:

- Whether rent should be paid

- Who is responsible for utilities

- Whether the occupant may remain during probate

- Whether the occupant has a written or oral tenancy

- Whether the occupant is damaging the property

- Whether one heir’s occupancy is fair to the other beneficiaries

These situations should be reviewed with the estate attorney and, when appropriate, an attorney familiar with landlord-tenant law.

What If the House Has a Reverse Mortgage?

A reverse mortgage can create an urgent deadline.

After the last borrower dies, the loan generally becomes due and payable. The heirs or estate may need to sell the home, refinance it, pay off the loan, or pursue another permitted resolution.

For an FHA-insured Home Equity Conversion Mortgage, extensions may be available when the estate or heirs provide satisfactory documentation showing that they are actively working toward a sale or other resolution. Extensions are not automatic, so the servicer should be contacted promptly. (HUD.gov)

Important steps include:

- Notify the loan servicer

- Request a current payoff statement

- Determine whether an eligible non-borrowing spouse is involved

- Confirm deadlines in writing

- Keep records of all communications

- Provide requested documentation promptly

- Obtain an estimate of the home’s current value

Waiting too long can reduce the estate’s options and put the remaining equity at risk.

What If Property Taxes Are Behind?

Delinquent property taxes do not disappear after the owner’s death.

Penalties and interest may continue to accumulate. If the delinquency remains unresolved for a long period, the property may eventually become subject to the county’s tax-sale process.

The personal representative should contact the county tax collector to confirm:

- The amount currently due

- Whether the property is tax-defaulted

- Applicable penalties and interest

- Available payment or redemption options

- Important future deadlines

Selling the home may be one way to pay the delinquent taxes, but the estate should first understand the full financial situation and available alternatives.

What If the House Needs Major Repairs?

Many inherited Bay Area homes have been owned for 30, 40, or 50 years and may not have been updated recently.

Common issues include:

- Old electrical panels or wiring

- Roof leaks

- Foundation movement

- Plumbing problems

- Termite or dry-rot damage

- Outdated kitchens and bathrooms

- Unpermitted additions

- Mold or water damage

- Excessive personal belongings

- Code violations

- Fire or smoke damage

The estate does not necessarily have to renovate the house before selling it.

The correct decision depends on the expected increase in sale price compared with the repair cost, holding time, construction risk, and available estate funds.

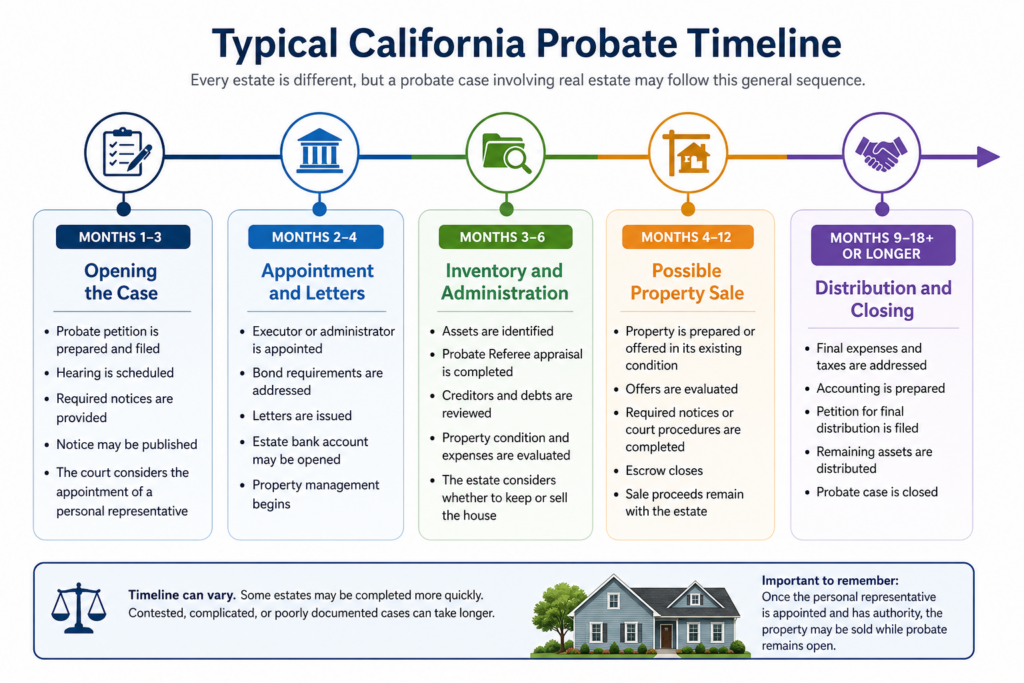

3. How Long Does California Probate Take?

According to the California Courts’ self-help guidance, a formal probate case typically takes approximately 9 to 18 months. Contested, complicated, or poorly documented cases can take longer. (Self-Help Guide to the California Courts)

That does not necessarily mean the estate must wait until the entire probate case is closed before selling the house.

Once the personal representative is appointed, receives the necessary Letters, and has the required authority, the property may often be sold while the probate case remains open.

The sale proceeds normally remain part of the estate until debts, expenses, taxes, and distribution requirements are addressed.

Typical California Probate Timeline

Every estate is different, but a probate case involving real estate may follow this general sequence:

Months 1–3: Opening the case

- Probate petition is prepared and filed

- Hearing is scheduled

- Required notices are provided

- Notice may be published

- The court considers the appointment of a personal representative

Months 2–4: Appointment and Letters

- Executor or administrator is appointed

- Bond requirements are addressed

- Letters are issued

- Estate bank account may be opened

- Property management begins

Months 3–6: Inventory and administration

- Assets are identified

- Probate Referee appraisal is completed

- Creditors and debts are reviewed

- Property condition and expenses are evaluated

- The estate considers whether to keep or sell the house

Months 4–12: Possible property sale

- Property is prepared or offered in its existing condition

- Offers are evaluated

- Required notices or court procedures are completed

- Escrow closes

- Sale proceeds remain with the estate

Months 9–18 or longer: Distribution and closing

- Final expenses and taxes are addressed

- Accounting is prepared

- Petition for final distribution is filed

- Remaining assets are distributed

- Probate case is closed

What Can Delay Probate?

Common delays include:

- Court backlogs

- Incomplete or incorrect filings

- Missing heirs

- Disputes among beneficiaries

- Will contests

- Difficulty locating assets

- Title defects

- Creditor claims

- Tax issues

- Problems obtaining insurance

- Reverse-mortgage deadlines

- Tenant or occupant disputes

- Major repairs

- Overpricing the property

- Court-confirmation requirements

The house itself can also delay the estate when family members postpone deciding what to do.

While the decision is delayed, the estate may continue paying the mortgage, property taxes, insurance, utilities, HOA dues, and maintenance.

Can a House Be Sold Before Probate Is Finished?

Yes, in many cases.

A probate house may often be sold after the personal representative has been appointed and received the necessary authority, even though the probate case itself remains open.

However, the transaction must follow the authority granted to the representative and any applicable notice, appraisal, court-confirmation, or sale requirements.

The estate attorney, title company, and escrow officer should review the representative’s authority before the property is listed or sold.

4. Common Challenges for Bay Area Executors and Families

Probate is not difficult only because of the court paperwork. The practical and emotional issues surrounding the house are often more challenging.

Multiple Heirs Disagree

One heir may want to keep the home. Another may want to sell immediately. A third may believe the house should be remodeled before it is sold.

Disagreement does not always mean the estate is unable to move forward.

The executor or administrator has a duty to act for the estate as a whole, not simply follow the preference of the loudest beneficiary. The representative should obtain legal advice, document the available options, and compare the likely financial consequences.

A useful comparison may include:

- Current as-is market value

- Expected value after repairs

- Estimated repair cost

- Time required for construction

- Monthly holding costs

- Direct-sale offers

- Expected listing expenses

- Likely net proceeds

- Risk of market changes

Providing family members with clear numbers can make the discussion less emotional and more practical.

The Executor Lives Outside the Bay Area

An out-of-state executor may find it difficult to:

- Inspect the property

- Meet contractors

- Remove belongings

- Coordinate repairs

- Handle tenants

- Maintain the yard

- Respond to code-enforcement notices

- Provide access to appraisers or buyers

A local real estate professional can help coordinate inspections, vendors, estate-sale companies, cleanout crews, contractors, escrow, and title work.

The executor should still control the important decisions, but many of the local tasks can be delegated.

The House Is Filled With Personal Belongings

A home occupied for decades may contain furniture, documents, photographs, collectibles, tools, clothing, and other personal items.

The family should not rush to discard everything.

Before a cleanout:

- Locate estate-planning and financial records

- Identify valuables and family keepsakes

- Confirm whether specific items were left to particular beneficiaries

- Photograph the contents

- Ask the attorney whether an inventory is needed

- Consider an estate sale, donation, or professional cleanout

When selling directly, it may be possible to leave unwanted items behind. When listing on the open market, clearing some or all of the contents may make the home easier to inspect, photograph, and show.

One Heir Lives in the Property

Occupancy by an heir can become a sensitive issue.

Questions may include:

- Is the heir paying rent?

- Is the heir maintaining the property?

- Is the heir preventing access?

- Should the heir receive a credit for expenses paid?

- Should the estate receive an occupancy payment?

- Does the occupant have tenant protections?

- Can the property be shown while occupied?

The executor should avoid informal promises that could create conflict later. An attorney can help the estate establish appropriate occupancy terms or determine what steps are legally available.

The House Has Tenants

A tenant-occupied inherited property requires special care, especially in Bay Area jurisdictions with local rent-control or eviction rules.

The estate generally takes ownership subject to the existing tenancy. Selling the property does not automatically end the tenant’s rights.

Before making promises to a buyer, the estate should confirm:

- The lease terms

- Current rent

- Security deposit

- Payment history

- Local rent-control status

- Local eviction restrictions

- Whether any relocation payment could apply

- Whether the tenant will cooperate with showings

A tenant-occupied home can still be sold, but the strategy and likely buyer pool may be different from those for a vacant home.

The House Has Deferred Maintenance or Code Violations

The existence of repairs or violations does not necessarily prevent a sale.

Depending on the problem, the estate may:

- Correct the issue before selling

- Obtain bids and disclose the condition

- List the home as-is

- Sell directly to a buyer willing to take on the work

- Negotiate responsibility for compliance

- Work with the city on a reasonable timeline

The representative should understand whether any fines, liens, permits, or deadlines are attached to the property before accepting an offer.

5. Proposition 19 and Tax Considerations

Taxes are one of the most misunderstood parts of inheriting a California home.

Property taxes, capital gains taxes, estate taxes, and inheritance taxes are separate issues. The outcome depends on the property, date of death, ownership, use of the home, and the people receiving it.

A CPA, tax attorney, and county assessor should be consulted for advice on a specific case.

How Proposition 19 Affects an Inherited Home

Proposition 19 significantly changed California’s parent-child property-tax exclusion for transfers occurring on or after February 16, 2021.

Under the current rules, the exclusion is generally limited to a qualifying family home or family farm. For a family home, the property generally must have been the parent’s principal residence and must become the eligible child’s principal residence. The required claims must also be filed with the county assessor. (California State Board of Equalization)

An inherited rental property, second home, or vacation property generally does not qualify for this parent-child exclusion merely because it passes from a parent to a child. (California State Board of Equalization)

Why Proposition 19 Matters in the Bay Area

Many Bay Area homeowners bought their properties decades ago and have taxable values far below today’s market prices.

Consider this simplified illustration:

- Parent’s current assessed value: $250,000

- Approximate current market value: $1,800,000

- Child inherits the property but does not qualify for the exclusion

If the property is reassessed near its current market value, the annual property-tax bill could increase substantially.

The exact tax is not calculated by simply multiplying the market value by one universal rate. Local assessments, bonds, exemptions, and the assessor’s determination can affect the final bill.

Before deciding to keep the home as a rental or second residence, the family should obtain an estimate of the likely new assessed value and annual property tax.

Does California Have an Inheritance Tax?

California does not generally impose a state inheritance tax simply because someone receives inherited property.

The inheritance itself is also generally not included as income on a California personal income-tax return. However, income later produced by the inherited asset—such as rent, interest, or taxable gain from a sale—may be taxable. (State of California Franchise Tax Board)

Very large estates may still face federal estate-tax considerations.

What Is a Step-Up in Basis?

Inherited property generally receives a new tax basis based on its fair market value at the date of death, subject to applicable tax rules and exceptions. (State of California Franchise Tax Board)

For example:

- Original purchase price: $150,000

- Fair market value at date of death: $1,800,000

- Sale price several months later: $1,850,000

The taxable gain is not necessarily calculated from the original $150,000 purchase price. The new basis may be approximately $1,800,000, with adjustments for selling expenses, improvements, and other applicable items.

Because the property increased by only $50,000 after the date of death in this simplified example, the taxable gain may be much smaller than the family initially expected.

However, the actual calculation can vary based on:

- The date-of-death valuation

- Whether an alternate valuation applies

- Improvements after death

- Depreciation

- Rental use

- Selling expenses

- Whether the estate or beneficiaries sell the home

- State and federal tax treatment

A tax professional should calculate the basis and potential gain before the sale is reported.

Property-Tax Basis and Income-Tax Basis Are Different

This is an important distinction.

Property-tax basis determines the assessed value used by the county to calculate annual property taxes.

Income-tax basis is used to calculate gain or loss when the property is sold.

Proposition 19 concerns property-tax reassessment. The step-up in basis concerns income-tax calculations.

A family can receive a step-up in income-tax basis while still facing a major increase in annual property taxes.

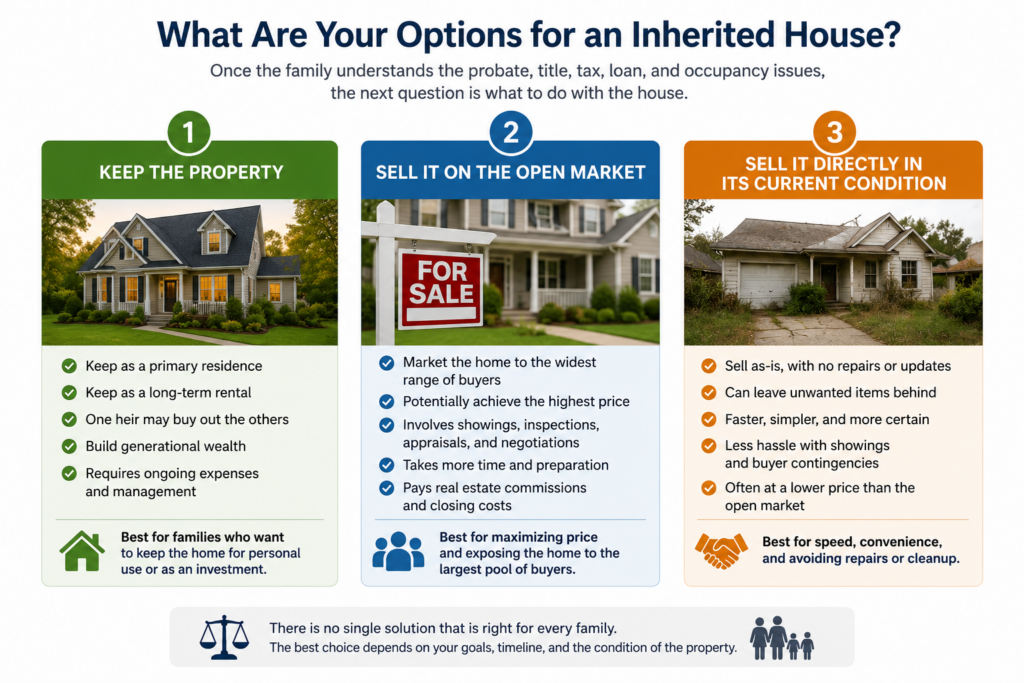

6. Options for an Inherited Bay Area House

Once the family understands the probate, title, tax, loan, and occupancy issues, the next question is what to do with the house.

There are generally three broad options:

- Keep the property

- Sell it on the open market

- Sell it directly in its current condition

The best choice depends on the family’s goals, the condition of the house, available cash, time constraints, tax consequences, and the needs of the beneficiaries.

Option 1: Keep the Property

The family may decide to keep the home as a residence or rental.

This may make sense when:

- An heir genuinely wants to live there

- The property works as a long-term rental

- The family can afford the ongoing expenses

- The heirs agree on ownership and management

- One heir can buy out the others

- Financing is available

- The property-tax consequences are acceptable

Before keeping the home, consider:

- The new property-tax bill

- Mortgage or reverse-mortgage payoff

- Repairs and capital improvements

- Insurance

- Rental-management costs

- Local landlord-tenant rules

- Buyout terms for other beneficiaries

- Whether all heirs want to remain financially connected

Keeping the home can preserve a family asset, but it can also create years of disagreement if the ownership and responsibilities are not clearly structured.

Option 2: Sell on the Open Market

Listing the property on the Multiple Listing Service generally gives it exposure to the largest number of potential buyers.

This may produce the highest sale price when the home is in a desirable location and there is strong buyer demand.

The estate does not always have to complete a major renovation before listing.

Possible listing strategies include:

- Full renovation and staging

- Limited repairs and cosmetic improvements

- Cleanout without major repairs

- Selling on the MLS in its current condition

- Marketing to contractors, investors, and owner-occupants

- Selling with tenants or occupants in place

Advantages of open-market exposure may include:

- More potential buyers

- Competitive bidding

- Greater price discovery

- Opportunity to attract owner-occupants

- Potentially higher gross sale price

Potential disadvantages may include:

- Preparation expenses

- Real estate commissions

- Buyer financing and appraisal risk

- Inspection contingencies

- Showings and open houses

- Longer closing time

- Possible repair negotiations

- Uncertainty over the final net proceeds

An open-market listing may be the best financial choice when the estate has time, the property can be marketed effectively, and maximizing the price is the primary goal.

Option 3: Sell Directly in As-Is Condition

A direct sale may be appropriate when the estate values speed, simplicity, or certainty more than achieving the highest possible retail price.

A direct buyer may be willing to purchase the home:

- Without repairs

- Without staging

- Without a full cleanout

- With unwanted belongings left behind

- With code or maintenance issues

- On a flexible closing date

- Without a buyer loan contingency

Advantages may include:

- Less preparation

- Fewer showings

- Faster inspections and decisions

- Greater closing certainty

- Flexible possession terms

- Reduced risk of repair demands

- Ability to leave unwanted items

The tradeoff is that a direct investor offer will often be lower than the price that might be achieved through full open-market exposure.

That does not automatically make the offer good or bad. The estate should compare the net proceeds and risk, not only the headline price.

How to Compare a Direct Offer With a Listing

A proper comparison should include:

- Expected sale price

- Real estate commissions

- Buyer credits

- Escrow and title costs

- Repair and preparation costs

- Cleanout and staging expenses

- Monthly holding costs

- Buyer financing risk

- Inspection risk

- Appraisal risk

- Probability of closing

- Time until the estate receives the proceeds

Example

Open-market sale

- Expected price: $1,200,000

- Commissions and closing expenses: $65,000

- Repairs, cleanup, and staging: $100,000

- Three months of holding costs: $15,000

- Estimated net before other estate obligations: $1,020,000

Direct as-is sale

- Offer price: $900,000

- No repair or staging expense

- Limited seller closing expenses

- Shorter holding period

- Estimated net: approximately $900,000

In this simplified example, the open-market sale may still produce more money, but the difference in net proceeds is much smaller than the $300,000 difference between the two offer prices.

The representative must decide whether the additional time, work, expense, and risk are justified by the expected increase in net proceeds.

Selling As-Is Does Not Eliminate Disclosure Responsibilities

“As-is” generally means that the seller does not agree in advance to make repairs.

It does not necessarily mean the estate can conceal known material facts or ignore applicable disclosure obligations.

The required disclosures can depend on:

- Whether the seller is an estate or trust

- Whether the representative occupied the property

- The type of transaction

- The property

- Local requirements

- Known conditions

The estate should obtain guidance from the attorney and real estate professional regarding the disclosures that apply.

7. Frequently Asked Questions About Probate and Inherited Houses

Does a will avoid probate?

Not necessarily. A will directs the distribution of property and names a preferred executor, but individually owned assets may still require probate.

Can an inherited house be sold before probate is finished?

Often, yes. The personal representative generally must first be appointed, receive Letters, and have the necessary authority. The sale proceeds remain part of the estate until distribution is authorized.

Can the executor sell the house without every heir signing?

The answer depends on the executor’s authority, the will, court orders, and the circumstances. A properly appointed personal representative may have authority to sell estate property even when a beneficiary disagrees, but the representative must follow California law and fiduciary duties.

What if one heir refuses to cooperate?

The executor should document the disagreement and consult the probate attorney. A beneficiary’s objection may not automatically prevent a sale, but it can create delay or litigation.

Who pays the mortgage and property taxes during probate?

These are generally estate expenses. If the estate lacks cash, a family member may sometimes advance funds and later request reimbursement, but this should be documented and discussed with the attorney.

Can an heir live in the property during probate?

Possibly, but the arrangement should be reviewed carefully. The executor must consider the interests of all beneficiaries and issues such as rent, expenses, property access, and maintenance.

Can a beneficiary buy the house from the estate?

Possibly. The transaction should be handled transparently and at an appropriate value. Additional consent, notice, appraisal, or court procedures may be necessary.

Does the house have to be empty before it is sold?

No. Some buyers will purchase a home with furniture, belongings, debris, or tenants still present. However, occupancy and personal-property issues should be disclosed and clearly addressed in the contract.

Does the estate have to repair the house?

Not necessarily. The estate can compare renovating, completing limited repairs, listing as-is, and selling directly.

Can a probate property be listed on the MLS as-is?

Yes. “As-is” and “MLS listing” are not opposites. A property can be exposed to the open market without the estate completing major repairs.

How is a probate house valued?

The Probate Referee may provide a date-of-death appraisal for estate purposes. A Realtor® can provide a current comparative market analysis, and a licensed appraiser can provide a separate appraisal when appropriate.

What happens if the house has a reverse mortgage?

The servicer should be contacted immediately. The heirs or estate may need to sell, refinance, repay the loan, or pursue another permitted option. Do not assume extensions will be granted automatically.

Does Proposition 19 apply to inherited rental property?

An inherited rental property generally does not qualify for the current parent-child exclusion merely because it passes from parent to child. The county assessor and a tax professional should review the specific facts.

How long does a probate sale take?

The real estate transaction itself may close in a normal escrow period after the representative has authority and all required procedures are satisfied. The overall probate case typically takes much longer.

Can an out-of-state executor sell a California house?

Yes, in many cases. Much of the transaction can be coordinated remotely, although local professionals may be needed to secure, inspect, clean, repair, and market the property.

What if the property has tenants?

The tenancy generally continues after the owner’s death. The estate must comply with the lease and applicable state and local laws. Legal advice is especially important in rent-controlled Bay Area jurisdictions.

8. Help With a Bay Area Probate or Inherited House

Managing an inherited home is not only a legal process. It is also a real estate, financial, and family decision.

Some families need the highest price the open market can produce. Others value a straightforward as-is sale with no repairs, cleanout, staging, or extended buyer financing process.

My role is to help you understand both options.

I’m Eddie Lam, a California Realtor® with eXp Realty of California. I have worked in Bay Area real estate since 2008.

My experience includes properties involving:

- Probate and inherited ownership

- Living trusts

- Reverse mortgages

- Delinquent property taxes

- Deferred maintenance

- Code violations

- Fire damage

- Tenants and occupants

- Out-of-state owners

- Properties requiring substantial cleanup or repairs

Because I work as both a Realtor® and an investor, I can help the estate compare different approaches instead of automatically steering every property toward the same solution.

Depending on your circumstances, I can help you:

- Review the home’s current condition

- Estimate its likely as-is market value

- Evaluate whether repairs are worthwhile

- Compare a traditional listing with a direct sale

- Estimate likely net proceeds

- Coordinate with escrow and title professionals

- Assist with local vendors, cleanout companies, and contractors

- Market the home to the open market

- Discuss a possible direct purchase

- Work with your probate or estate attorney as needed

I help executors, trustees, heirs, and families with inherited properties throughout San Mateo County, Santa Clara County, Alameda County, San Francisco County, Contra Costa County, and surrounding Bay Area communities.

There is no obligation to make an immediate decision.

Sometimes the most useful first step is simply to understand the property’s condition, likely value, expenses, and available options.

Contact or text Eddie Lam at 650-980-9819 to discuss your Bay Area inherited property, request an as-is value review, compare selling options, or ask questions about the real estate side of the probate process.

What Do You Have To Lose? Get Started Now…

We buy houses in ANY CONDITION in CA. There are no commissions or fees and no obligation whatsoever. Start below by giving us a bit of information about your property or call 650-980-9819…

Important Disclaimer

This article is provided for general informational purposes only. It is not legal, tax, accounting, insurance, or financial advice.

Probate, trust administration, title, taxation, reverse mortgages, property reassessment, landlord-tenant rules, and real estate disclosures depend on the specific facts of each case and are subject to change.

Consult an appropriately qualified probate or estate-planning attorney, CPA or tax professional, county assessor, insurance professional, loan servicer, and other advisers regarding your circumstances.

The article now functions as a true Carrot authority page: it educates first, addresses the reader’s practical problems, presents the choices fairly, and introduces your services after trust has been established. The core probate timeline, Proposition 19, inherited-basis, and reverse-mortgage statements were checked against official California Courts, Board of Equalization, Franchise Tax Board, and HUD guidance. (Self-Help Guide to the California Courts)