If you’ve inherited a house with a reverse mortgage, you may be wondering what happens next. Can you keep the home? Do you have to sell it? How much time do you have? This guide explains how reverse mortgages work after the homeowner passes away, what options heirs have, and the steps you can take to make an informed decision.

In This Guide

- What Is a Reverse Mortgage?

- Who Qualifies?

- Can You Sell a House With a Reverse Mortgage?

- Can You Inherit a House With a Reverse Mortgage?

- What Happens After the Homeowner Passes Away?

- How Does Escrow Work With a Reverse Mortgage

- Timeline After Death

- Does Probate Affect a Reverse Mortgage?

- California Proposition 19

- Frequently Asked Questions

- Call Eddie

Reverse Mortgage: What Happens After the Homeowner Passes Away?

If you’ve recently inherited a home with a reverse mortgage, you’re probably asking one of these questions:

- Can I keep the house?

- Do I have to sell it?

- How much time do I have?

- What happens if I can’t pay off the loan?

You’re not alone.

Many families first learn about the reverse mortgage only after a parent or loved one passes away. The good news is that you usually have several options, and understanding them early can help you avoid unnecessary stress. I’ve worked with Bay Area families dealing with inherited properties, probate, reverse mortgages, tax-delinquent homes, and other situations where timing and clear information are important.

This guide explains how reverse mortgages work, what happens after the borrower passes away, and the choices available to heirs.

What Is a Reverse Mortgage?

A reverse mortgage is a loan available to homeowners who are at least 62 years old. Instead of making monthly mortgage payments, the homeowner borrows against the equity in the home.

Unlike a traditional mortgage:

- No required monthly mortgage payments are made.

- Interest and loan costs are added to the loan balance over time.

- The loan is generally repaid when the homeowner permanently moves out, sells the home, or passes away.

The property must be the homeowner’s primary residence. Reverse mortgages are generally not available for rental or investment properties.

Many retirees use a reverse mortgage to supplement retirement income, pay medical expenses, or improve cash flow while remaining in their home.

Who Qualifies for a Reverse Mortgage?

In general, homeowners may qualify if they:

- Are at least 62 years old.

- Live in the property as their primary residence.

- Have sufficient equity in the home.

- Continue paying property taxes, homeowners insurance, and maintaining the property.

The amount available depends on factors such as:

- Age of the youngest borrower

- Current interest rates

- Home value

- Existing mortgage balance

If there is an existing mortgage, it is typically paid off first using the reverse mortgage proceeds.

Can I Sell a House That Has a Reverse Mortgage?

Yes.

A reverse mortgage does not prevent you from selling the home.

In fact, selling the property is one of the most common ways to repay the loan.

During escrow, the reverse mortgage lender provides a payoff statement. The loan is paid from the sale proceeds, and any remaining equity belongs to the homeowner or the estate.

Many homeowners choose to sell because they are:

- Downsizing

- Moving into assisted living

- Relocating closer to family

- No longer able to maintain the property

Can I Inherit a House That Has a Reverse Mortgage?

Yes.

A reverse mortgage does not prevent heirs from inheriting the property.

However, the reverse mortgage loan does not disappear.

When the homeowner passes away, the loan becomes due, and the heirs must decide what to do next.

Most families choose one of four options:

Option 1 — Sell the Home

This is the most common solution.

The reverse mortgage is paid off during escrow, and any remaining equity belongs to the estate or heirs.

Option 2 — Keep the Home

If an heir wants to keep the property, they can usually refinance the reverse mortgage into a traditional mortgage, provided they qualify for financing.

Option 3 — Pay Off the Loan

Some families simply pay off the reverse mortgage using available cash or other assets.

Option 4 — Walk Away

Reverse mortgages are generally non-recourse loans.

If the loan balance exceeds the home’s value, heirs are typically not personally responsible for the difference. The lender’s recovery is generally limited to the value of the property.

| Option | Best For | Pros | Cons |

|---|---|---|---|

| Sell | Most heirs | Fastest solution | Must move |

| Refinance | Keep the home | Retain ownership | Must qualify |

| Pay Off | Available cash | No new loan | Requires funds |

| Walk Away | Underwater property | No personal liability | Lose the home |

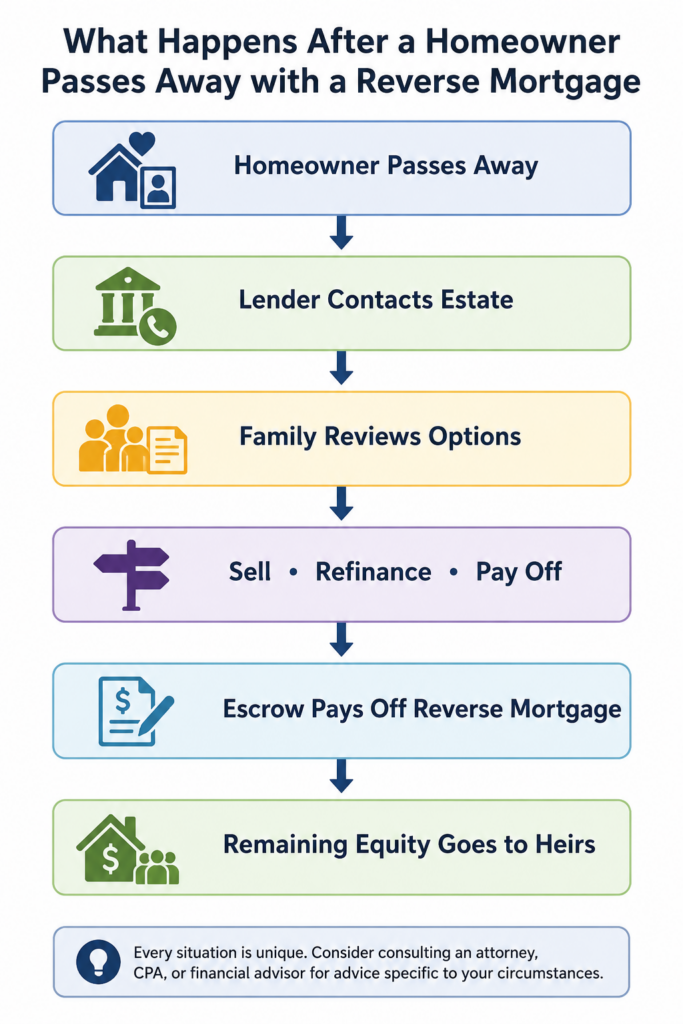

What Happens After the Homeowner Passes Away?

Once the last borrower passes away or permanently leaves the home, the reverse mortgage becomes due.

The lender will usually contact the estate or heirs and begin the payoff process.

Families generally have several months to determine their next steps.

Typical timeline:

- The lender notifies the estate.

- The heirs evaluate the property’s value and the loan balance.

- The family decides whether to sell, refinance, or pay off the loan.

- If additional time is needed, extensions may sometimes be available, especially when the family is actively making progress toward resolving the loan.

Because interest continues to accrue, delaying a decision may reduce the remaining equity available to the family.

Timeline After the Homeowner Passes Away

When the last borrower on a reverse mortgage passes away (or permanently moves out of the home), the loan becomes due. While every situation is different, the process generally follows this timeline.

Step 1: The Lender Is Notified

Once the lender learns that the homeowner has passed away, it will begin the process of resolving the reverse mortgage. This may happen after receiving a death certificate or through other notification.

Step 2: The Estate or Heirs Receive a Notice

The lender will typically contact the executor, trustee, or heirs to explain that the reverse mortgage has become due and outline the available options.

Step 3: The Family Decides What to Do

Most families choose one of the following options:

- Sell the property and use the sale proceeds to pay off the reverse mortgage.

- Refinance the reverse mortgage into a traditional mortgage and keep the home.

- Pay off the loan using available cash or other assets.

- In some situations, choose not to keep the property.

This is often the most important decision because interest continues to accrue while the loan remains outstanding.

Step 4: The Property Is Sold or the Loan Is Paid Off

If the family decides to sell the home, the reverse mortgage is typically paid off through escrow at the close of the sale. Any remaining equity belongs to the estate or heirs.

If the family decides to keep the property, the reverse mortgage must usually be satisfied through refinancing or another source of funds.

How Much Time Do Heirs Have?

In many cases, heirs initially have about six months to resolve the reverse mortgage. If additional time is needed, the lender may grant extensions when the family is actively working toward a resolution, such as listing the property for sale or completing probate.

Because every loan is different, it’s important to communicate with the loan servicer as early as possible rather than waiting until the deadline approaches.

How Does Escrow Work When Selling a House with a Reverse Mortgage?

Selling a home with a reverse mortgage is very similar to a traditional home sale.

During escrow:

- The title company orders the reverse mortgage payoff.

- The lender provides the payoff amount.

- The loan is paid from the sale proceeds at closing.

- Any remaining funds are distributed to the seller or the estate.

If probate is required, the timing may depend on the probate process and court requirements.

If the property is held in a living trust, the sale is often more straightforward because probate may be avoided.

Every situation is different, especially when multiple heirs, probate, trusts, or title issues are involved.

Does Probate Affect a Reverse Mortgage?

It can.

Whether probate is required depends on how the property is titled, not on the reverse mortgage itself.

If the Home Is Held in a Living Trust

Many California homeowners place their home in a revocable living trust.

When the homeowner passes away, the successor trustee can often sell or transfer the property without going through probate. This usually makes resolving the reverse mortgage faster and simpler.

If the Home Is Owned in the Individual’s Name

If the property was not placed in a trust or transferred using another estate planning method, probate may be required before the home can be sold.

Probate can take several months—or sometimes longer depending on the circumstances.

Because reverse mortgages continue to accrue interest, it’s important for the executor or heirs to keep the lender informed if probate is underway. In some cases, the lender may allow additional time while the estate is actively progressing through the probate process.

Every Situation Is Different

Factors such as multiple heirs, disputes among family members, title issues, or court delays can all affect the timeline.

If you’re unsure whether probate will be required, it is usually a good idea to speak with a probate attorney before making any decisions.

If your goal is simply to understand your options for selling the property, I can also help explain how the sale process works while probate is pending.

California Proposition 19 and Inherited Homes

One issue that many families overlook is California Proposition 19, which may affect the property’s annual property taxes after inheritance.

Before deciding whether to keep or sell an inherited home, it’s important to understand how Proposition 19 may impact your long-term costs.

What Changed Under Proposition 19?

In many situations, children who inherit a home no longer automatically keep their parents’ low property tax assessment.

If the inherited property does not qualify for one of the available exclusions, the county assessor may reassess the property at its current market value.

This can result in a significant increase in annual property taxes.

Why Does This Matter?

For some families, the increased property taxes make it much more expensive to keep the home.

When combined with:

- paying off the reverse mortgage,

- ongoing maintenance,

- insurance,

- and future repair costs,

keeping the property may not be financially practical.

Others may decide that keeping the home still makes sense because of family circumstances or long-term investment goals.

Understand the Numbers Before Making a Decision

Every family’s situation is different.

Before deciding whether to keep or sell an inherited property, it’s a good idea to understand:

- The current market value of the home.

- The reverse mortgage payoff amount.

- Whether Proposition 19 may increase future property taxes.

- The estimated costs of owning the property going forward.

Taking the time to review these factors can help you make a more informed decision and avoid unexpected expenses later.

Frequently Asked Questions

Will I owe money if the house sells for less than the reverse mortgage balance?

Generally, no. Most reverse mortgages are FHA-insured Home Equity Conversion Mortgages (HECMs), which are non-recourse loans. That means if the home sells for less than the loan balance, neither you nor the estate is typically responsible for paying the difference. The lender’s recovery is generally limited to the value of the property.

Can I inherit a house with a reverse mortgage?

Yes. A reverse mortgage does not prevent you from inheriting a home. However, you also inherit the responsibility of resolving the reverse mortgage loan. Once the last borrower passes away, the loan becomes due. As an heir, you generally have several options: sell the home, refinance the loan to keep the property, pay off the balance using other funds, or allow the lender to take the property if you decide not to keep it. The best option depends on your financial situation and your long-term goals.

Do I have to sell the house?

No. Selling the home is the most common solution, but it is not the only one. If you want to keep the property, you may be able to refinance the reverse mortgage into a traditional mortgage or pay off the loan with other assets. Every family’s situation is different, and understanding the property’s value, the loan balance, and your financial goals can help determine the best option.

Can I keep the house?

Yes, provided the reverse mortgage is paid off. Most heirs keep the home by obtaining a new mortgage, paying off the reverse mortgage with cash, or using other available assets. Because reverse mortgages cannot simply be “assumed” like some traditional mortgages, heirs usually need to satisfy the existing loan before taking full ownership.

How long do I have after someone dies?

The timeline varies depending on the loan and individual circumstances. In many cases, heirs initially have about six months to resolve the reverse mortgage, and additional extensions may be available if the family is actively working toward a sale or refinancing. It is important to communicate with the loan servicer as early as possible rather than waiting until the deadline approaches.

Can I sell before probate is finished?

Sometimes. If the property is held in a living trust, probate may not be required, allowing the sale to proceed more quickly. If probate is required, the personal representative may need court authority before the property can be sold. Every estate is different, so it is best to consult with a probate attorney regarding your specific situation.

Who pays property taxes?

Property taxes remain the responsibility of the property owner or the estate until the property is sold or transferred. Even after the homeowner passes away, property taxes, insurance, utilities, and maintenance should continue to be paid to avoid additional problems during the estate administration.

Can the lender foreclose?

Yes, but foreclosure is generally not the lender’s first choice. If the reverse mortgage is not paid off and no progress is being made toward selling or refinancing the property, the lender may eventually begin foreclosure proceedings. Staying in communication with the lender and demonstrating that the estate is actively resolving the loan can often help avoid unnecessary complications.

What if there are multiple heirs?

When there are multiple heirs, everyone should understand the available options before making a decision. Sometimes all heirs agree to sell the property and divide the remaining proceeds. In other situations, one heir may wish to keep the home while the others prefer to sell. Open communication is important, and legal advice may be necessary if disagreements arise.

Can an heir buy out the other heirs?

Yes. This is a fairly common solution. One heir may purchase the interests of the other heirs and refinance the reverse mortgage at the same time. This allows the property to remain in the family while providing the other beneficiaries with their share of the estate.

What if the loan is larger than the home’s value?

Most reverse mortgages are non-recourse loans. This means neither the heirs nor the estate are generally responsible for paying any amount above the value of the home. If the loan balance exceeds the home’s value, the lender’s recovery is typically limited to the property itself.

Can I sell the house as-is?

Yes. Many inherited homes are sold in their current condition without making repairs or renovations. Depending on your goals, you may choose to list the property on the open market or sell it directly to a buyer who purchases homes in as-is condition.

Does the house have to be empty before selling?

Not necessarily. Some homes are sold after the family has removed all personal belongings, while others are sold with remaining contents. The best approach depends on the buyer, the condition of the property, and the type of sale. If the home contains a lifetime of belongings, it’s often helpful to develop a plan for sorting, donating, or disposing of items before closing.

Can I use the proceeds to pay estate expenses?

Yes. After the reverse mortgage, closing costs, and any other liens are paid, the remaining proceeds become part of the estate. Depending on the estate’s circumstances, those funds may be used to pay valid estate expenses, debts, taxes, or distributions to beneficiaries before the remaining balance is distributed according to the will or California law.

What if the homeowner moved into assisted living before passing away?

A reverse mortgage requires the home to remain the borrower’s primary residence. If the homeowner permanently moves into assisted living or another long-term care facility, the reverse mortgage may become due even if the borrower is still living. Families should contact the loan servicer as soon as possible to understand the available options and applicable deadlines.

Does California Proposition 19 affect inherited homes?

It may. Proposition 19 changed the rules regarding inherited property tax assessments in California. Depending on how the property will be used and whether certain requirements are met, the home may be reassessed to its current market value, which could result in significantly higher annual property taxes. Before deciding whether to keep or sell an inherited property, it is important to understand how Proposition 19 may affect your situation. For a more detailed explanation, please see my California Proposition 19 guide.This is an important consideration before deciding whether to keep or sell the home.

Need Help Understanding Your Options?

Every reverse mortgage situation is different.

Some families decide to sell the home.

Others refinance and keep it.

Some simply want to understand what the property is worth before making a decision.

If you’re dealing with an inherited home, a reverse mortgage, probate, or simply aren’t sure what to do next, I’d be happy to discuss your situation.

There is absolutely no obligation and no pressure. Many of the families I speak with aren’t looking for an investor—they’re simply trying to understand what happens next. My goal is to help explain the process so they can make an informed decision.

You don’t have to decide today. Many families simply want to understand their options before making any decisions. If that’s where you are, I’m happy to answer your questions and explain the process. Call or text me at 650-980-9819, or use the contact form below to discuss your situation.

This article is for general informational purposes and is not legal or tax advice. Every reverse mortgage situation is unique. Consider consulting an attorney, CPA, or financial advisor for advice specific to your circumstances.

Let’s Talk About Your Options

Whether you sell to me, list with an agent, or simply want to understand your options, I’m happy to help.